The Ideal Portfolio:

Asset allocation matters.

Behavioral temperament really matters.

“Investor psychology tends to oscillate wildly between “flawless” and “hopeless” because they are reacting to short-term price movements. In the real world, things tend to move between pretty good and not so good.”

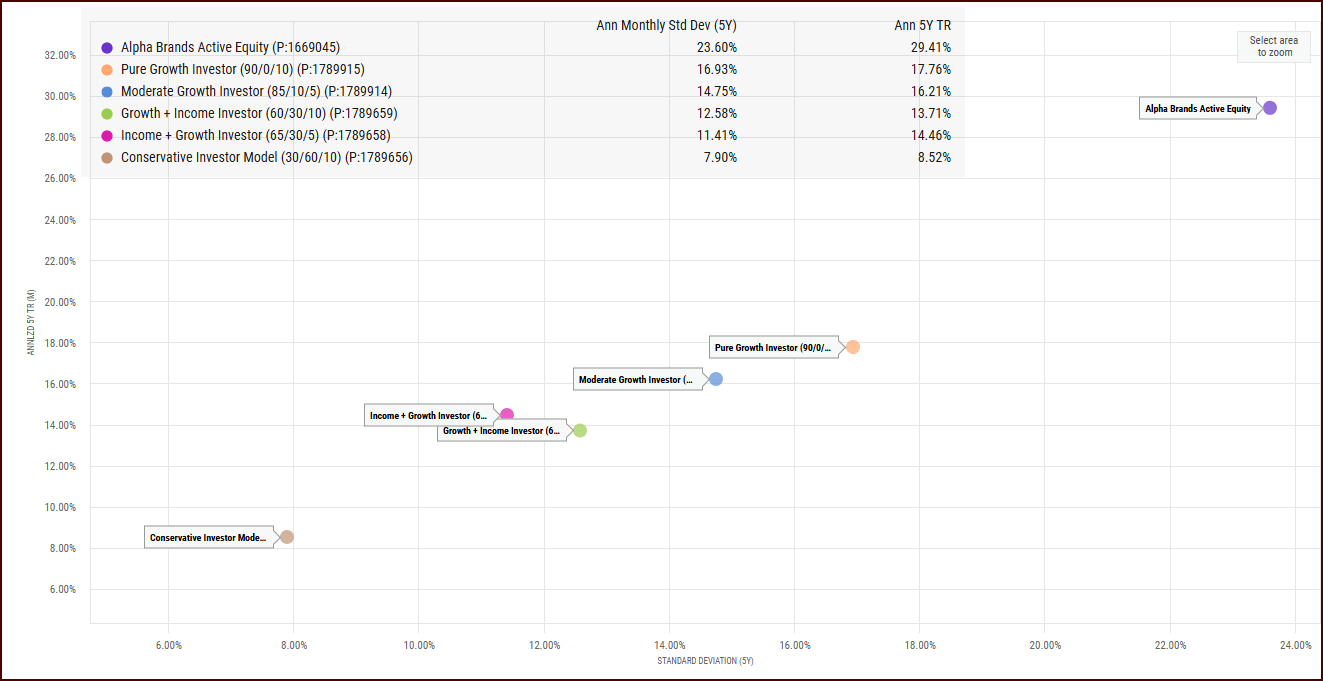

Every investor is unique. Every investor has different needs and risk tolerances. There is no “perfect” industry portfolio, no matter what Morningstar tells you. There are a handful of vital pieces of the puzzle that help to drive investment success. The image below should help set the stage for a deeper conversation that should help you and your advisor identify an ideal asset allocation that meets your specific needs.

The time you commit to invest + the total cost of investing + the base level of risk you are comfortable taking + the type of investments you choose + your behavioral temperament + your ability to think as a contrarian during perceived extreme periods = the likelihood of having a strongly positive outcome. If you can manage this equation at scale as an advisor or an individual investor, you are doing something very special.

The 11 question discovery assessment below is designed to be used as a collaborative tool between an advisor and HNW investors (you can use it as a DIY investor too). The more investment discussions this process stimulates, the better. The most successful investors are those that are educated on what to expect over a full market cycle and why each investment has been implemented. When you know what you own and why, you are better able to cope with the inevitable volatility that public markets provide, while taking advantage of the volatility for the betterment of your long-term goals.

Let’s Build a Robust Portfolio:

Building the prudent investment portfolio requires some discovery. Everyone’s goals, expectations, and risk tolerances are different so please enjoy using the investment portfolio proposal generation tool below to help you build the framework for an institutional-caliber portfolio. There is no one way, or right way, to build a portfolio because we each have different biases and goals. Using proper asset allocation techniques, while implementing some “guardrails” to keep you on track can go a long way to helping you achieve your long-term goals. Thanks in advance for taking a few minutes to help create a better portfolio for you and your family. This should take no more than 3 minutes to complete. This is NOT financial advise and is meant to be an investor resource.

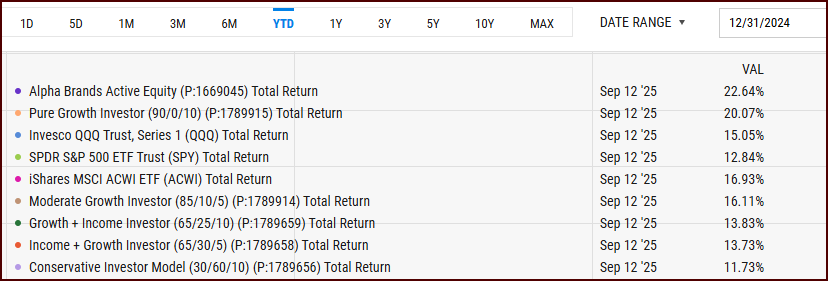

A word on the potential results. For illustrative purposes, I have spent hours researching the ETF universe for strong and sustainable performers that lead their peer group, created a list of important thematic ETF’s that appear quite timely in today’s market environment, and have created a handful of risk/reward based model portfolios for investors to consider. FWIW, here is my approach to building a portfolio.

The CORE:

The definition of CORE is: the single most important part of something.

The single most important driver of every major economy is household consumption. It’s $60T globally.

Brand loyalty: a key driver of purchase decisions so a basket of highly relevant brands is my chosen CORE.

The SATELLITES:

Identify important secular themes or mega trends that are worthy of investment. Gain some exposure.

#1: Tech & the AI revolution: Tech is an increasing part of our lives and AI will change everything in time.

#2: Second, third, and fourth derivative plays on AI: Private Equity, Credit & Infra are at center of buildout

Infrastructure Upgrades & Power Generation Expansion

US Utilities will spend $1.4T over the next 5 years to upgrade the grid

Massive funding needs to build & maintain this new AI infrastructure

Datacenters are expected to drive 50% of electricity grid capacity in 5 years

Traditional & renewable energy infrastructure upgrades

The US grid has 1300GW capacity today & predicted to be 2600GW in 5 years

A building, engineering, & construction boom that requires commodities of all kinds

#3: Aging society

Most of the world’s wealth is in the hands of an aging demographic & their assets are invested.

Older investors have less of a risk appetite and they like income & stability

#4: Active > Passive

The world has gone passive via mostly market cap weighted indexes, the over-concentration is epic

More passive = more idiosyncratic, active opportunities to exploit market inefficiencies

#5: Corporate financial engineering

In the U.S. alone, share buybacks are expected to exceed $1 trillion annually. This will only grow

AI and operating efficiencies will continue to drive higher multiples and profitability = buybacks grow

#6: Monetary madness

Governments around the world will continue to be fiscally irresponsible. Debt & deficits are exploding

Digital assets & hard assets continue to have a place in portfolios

#7: Fixed Income is different these days: no longer will it provide what it did in the past. Since rates bottomed, bond returns have largely been much lower and volatility has been 2x. Bonds might not be the best “safe asset that has an inverse correlation” to equities anymore. We need alternatives to traditional bonds