“From October 1, 2017 to September 20, 2019 ROKU stock returned roughly 304% versus the S&P 500 return of roughly 18%. It’s been a volatile ride but Roku has created a new market and the masses are just catching on to the story.”

COMPANY PROFILE

Roku’s streaming TV platform accounted for more than 30% of US sales of connected TV devices. That’s a powerful trend and wicked impressive installed base so far.

Strategy Analytics research: Now more than 41 million Roku-based devices in use, including Roku media streamers and Roku-based smart TVs, accounting for 15.2% of all media streaming devices. Strategy Analytics expects Roku’s installed base to grow to over 52 million by the year’s end, which would represent 18% of all connected media devices in the U.S., up from 15.2% in Q1. Roku is the operating system of single most prevalent piece of content we will consume as human beings for the next decade. Video is going to eat the world, with estimates coming in that 80% of the content we consume by 2020 will in fact be video.

Roku is the pick-axe to this move. It lists 11 TV makers as customers of its operating system and while we’re at it, 30%-40% of the streaming sticks as well. Roku TVs now account for one-in-three streaming TVs in the United States. Its growth is accelerating as the giants behind it fall further behind.

Its ads are more relevant than TV, viewing times and ad dollars are in total in-congruence, and will become congruent. Source: CML.com

From August 7, shareholder letter, Roku’s mission is simple:

When we founded Roku, we believed that one day all TV would be streamed, and that internet connectivity and modern software would revolutionize television for the consumer and the industry. It is exciting to see how much progress has been made.

We remain focused on reinforcing our position as the leading TV streaming platform in the U.S. and becoming a more international company. The growing scale and power of our platform continues to make Roku more desirable to users, content providers and advertisers. Our first-party relationships with consumers and sophisticated content promotion and advertising capabilities provide significant competitive advantages. We continue to invest in making it easier for viewers to find the content they love and for advertisers to reach a more relevant audience with innovative TV ad products. We believe we are uniquely positioned with respect to the secular shift in TV distribution and look forward to the second half of the year.

Roku pioneered streaming to the TV. We connect users to the streaming content they love, enable content publishers to build and monetize large audiences, and provide advertisers with unique capabilities to engage consumers. Roku streaming players and Roku TVTM models are available around the world through direct retail sales and licensing arrangements with TV OEMs and service operators. Roku is headquartered in Los Gatos, Calif. U.S.A.

If 25% ($250Billion) of a 1 trillion-dollar worldwide market is moving to streaming and ROKU gets 50% of cord cutters in the USA now, what does that mean for ROKU revenue potential? You see where I’m going with this? The U.S. market is projected to be roughly $75B per CML.com & Statista.

Summary of the opportunity via da Davidson tech conf interviews

Essential and neutral party to other streaming media players.

Competitor to Firestick from Amazon but a huge partner with Amazon Prime.

They are the leading streaming partner with significant market share.

Apple service will be on Roku but they also have their own AppleTV device.

More content on the platform = more engagement with consumers = more revenue sharing opportunities.

Disney Plus – its DTC but people will still access it via Roku if they already have Roku UI so they get paid .

All big players getting into OTT validates that all TV will be streamed over time - all but the big media players will realize their core strength is creation NOT distribution and monetization via ads,etc.

Roku continues to benefit from more content being created, this arms race for content allows them a robust offering for consumers given their market share.

Netflix-Revenue from them is not material. Why? Most people that come to Roku already have a Netflix account in US so the opportunity is INTL sub-adds.

They do rev shares with all partners when people spend money on platform so the more partners they have, the more rev shares they get.

Quarterly revenues can be lumpy because they have to report full revenue for new deals as accounting rule so making assumptions on a quarter are not a viable decision based on the ways they have to report revenue for new deals signed.

Roku channel – open to anyone who wants to put content on there. Because they know who’s watching, they can make better ad recs than TV providers.

There’s too many apps already, over time there will be less apps with content aggregation players gaining traction like Roku.

They sell 100% of the adds on Roku channel and 50/50 rev split so highly profitable and a huge focus and opportunity

They can monetize better than everyone because they have much better data about the demographics and in-app activities of users.

Advertising is key to roku and the # of advertisers and ad-load is going up exponentially to meet the number of eyeballs shifting to streaming.

Reiterate: Viewership well ahead of ad budgets so ad budgets will be forced to catch up to eyeballs so there’s a sling-shot in ad revenue adoption coming.

They serve ads dynamically and have better measurement tools for ad partners – that’s huge for more ad adoption.

They deliver better, more targeted ads so engagement is better for brands – more brands will come their way, its not debatable.

They empower content providers because they can help them monetize better on Roku platform – that makes partners get deeper in bed with them.

Most content providers are now realizing they aren’t really great at monetizing content, they are good at making content, they realize Roku is a better partner.

International expansion is absolutely coming, they wanted to build US first and perfect the model now building Intl capabilities.

They sell their Roku players for very low price with low input costs because of construction and chip advantages.

Neutral positioning is huge benefit.

Abilities on ad-side is key differentiator.

Intl – 11 OEM relationships now but Intl expansion is coming, its inevitable, deal news will be a future catalyst.

How they measure ROI on platform for partners – They have great behavioral data, your payment info on file so they check buying patterns across control groups a brand chooses to create campaigns for brands. This is much more robust than cable TV ad placement.

Baseball analogy – 1/3 of smart TVs sold are Roku TV’s so that’s 4/5 inning. The ad revenue opportunity is in the 1st or 2nd inning and the international opportunity is in pre-game to the first inning so there’s so much more game left to play making ROKU a much bigger opportunity than people think.

Remember – each quarterly report matters less than the massive shift in how consumers are consuming media. This is NOT going backward

Recent Earnings

We continue to execute well against our long-term strategic plan as the TV market shifts to streaming. In Q3, we beat our outlook for revenue, gross profit, and adjusted EBITDA. Our business momentum and competitive differentiation make Roku an essential partner for content publishers and advertisers. This is evident in the launch of major new streaming services on our platform and by the growth in the number of advertisers who work with Roku. We believe the dataxu acquisition will accelerate our platform’s advertising technology roadmap, strengthen our already industry-leading TV streaming platform and give us the opportunity to create an even more appealing offering for advertisers.

Q3 highlights - I’m not sure what else people can expect from this company - they are executing well and their opportunities keep expanding given massive increases of streaming hours on platform.

Total net revenue of $260.9 million, up 50% Year-over-Year (YoY);

Platform revenue of $179.3 million, up 79% YoY;

Active Accounts of 32.3 million, a net addition of 1.7 million over last quarter;

Streaming Hours increased 0.9 billion hours over last quarter, to 10.3 billion;

Average Revenue Per User (ARPU) of $22.58 (Trailing Twelve Months), up 30% YoY;

Gross Profit of $118.5 million, up 50% YoY; and

Roku monetized video ad impressions again more than doubled YoY.

Raising the revenue outlook for Q4 again from $485m to $492m at the mid-point & 46% growth to 49% growth and $1.106B FY revs.

We ended the quarter with $388 million of cash, cash equivalents, restricted cash and short-term investments.

Dataxu acquisition allows them to build bigger capabilities as the trend towards automated media buying accelerates. This will unlock more and bigger advertising opportunities for Roku.

Gross margins under a bit of pressure: Platform margins in range stated but mix shift to video ad business has lower gross margin average.

Q4 is always back-end loaded and subject to holiday shopping but the trend is unstoppable.

In August, we launched Kids & Family within The Roku Channel making it easy for families to find a wide selection of free and Premium Subscription content in one, easy-to-access destination.

There’s huge international growth opportunities and ROKU is entering that market slowly and methodically, it’s different than the USA. Heres the opportunity.

Important:

Everybody is getting into the content streaming business but how many streaming subscriptions can 1 family have?

Content spend has never been higher and eventually the economics will no longer be as attractive. Talent and infrastructure is already hard to come by. I’d rather own the platform that serves all the streaming options than be overweight the firms trying to out-spend peers to build strong libraries of content.

Q4 op-ex will rise due to stock based comp, hiring and Dataxu acquisition.

Outlook:

We are increasing our revenue and gross profit outlook for 2019 reflecting our strong Q3 performance and the inclusion of dataxu for part of Q4. Our raised revenue outlook midpoint of $1.106 billion represents roughly 49% year-over-year growth, up from 46% year- over-year in our prior outlook. We expect Platform revenue to represent roughly two-thirds of total revenue including approximately $13 million in revenue from dataxu. We are raising our total gross profit outlook for 2019 to roughly $492 million at the midpoint, up from roughly $485 million previously. We have updated our 2019 adjusted EBITDA outlook midpoint to $30 million from $35 million previously reflecting continued investment in the business as well as an approximately $5 million headwind to adjusted EBITDA in Q4 related to dataxu operations and dataxu acquisition related expenses.

Roku is THE essential partner for reaching a highly engaged TV streaming audience

According to eMarketer, around 56 million households in total will have canceled cable or satellite TV subscriptions by 2023. Approximately 1.7 million consumers cut the cord in Q3 alone. Our own research indicates that roughly 50% of U.S. cord cutters are Roku customers, and cord cutters who choose Roku products are highly satisfied with the decision and extremely unlikely to consider returning to a traditional pay TV subscription.

The growing number of major streaming services, increasing investment in original programming and related high-profile marketing campaigns are likely to reinforce consumer interest in moving from traditional pay TV to streaming – and to the Roku platform. Just last week Apple TV+ launched on our platform adding a desirable option for millions of Apple and Roku customers around the world. Disney+ and several new free ad-supported video on demand (AVOD) services coming to market are also expected to launch soon on our platform. Such new services will generate revenue for Roku when we promote their content to our customers, when customers sign up on our platform and when our customers view ads.

During Q3, we saw strong unit sales for both Roku TV and players. We continue to lead in smart TV operating system (OS) licensing as the #1 licensed TV OS in North America. We believe that Roku TV represented more than one in three smart TVs sold in the U.S. during the first nine months of the year.

In September, we introduced a new line up of streaming players for North America, Latin America and markets in Europe. These new players make streaming affordable with an entry price point of $29.99 MSRP for the redesigned Roku Express. Our goal is to drive scale and reach of the platform and we will do so by offering consumers exceptional devices and appealing prices rather thanoptimizing for hardware gross profit. We are pleased that our popular Roku Streaming Stick+ recently won the CNET Editor’s Choice Award for the third consecutive year and was once again deemed their favorite streamer overall.

Our competitive advantages support our international expansion

As we continue to lay the foundation for further international expansion, the key advantages that set us apart in the U.S. are expected to play an important role in new markets. Our purpose-built OS, engineering expertise, OEM partnerships, and free TV capabilities are among the many factors that we expect to contribute to our ability to attract content providers and consumers, and quickly build scale in new markets.

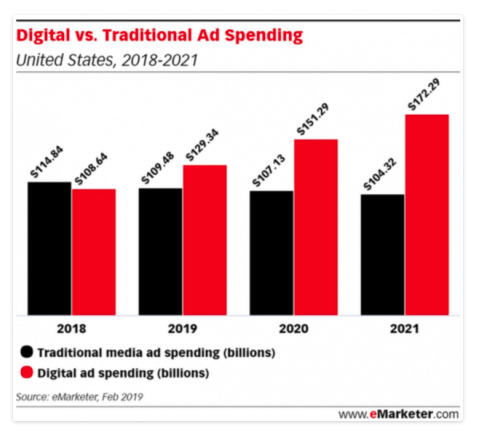

According to eMarketer, in the U.S., advertisers today spend more than $70 billion dollars on traditional linear TV and these dollars are still in the early stages of shifting to streaming. According to Magna Global, OTT accounts for 29 percent of U.S. TV viewing, but so far has only captured three percent of TV ad budgets. That gap is starting to close. For example, Magna Global forecasted $5 billion OTT ad spend for 2020. We believe that we are well positioned to benefit from this trend. Average annual advertiser spend is increasing on our platform and we are bringing in new advertisers. This includes strong interest in increasing ad effectiveness with anonymized first-party data and audience guarantees. Our sponsorships business – an ad product within the consumer user experience, such as a home screen takeover – is also growing faster than the overall business.

RISKS: With all the headline news around Trump and his tariffs, this stock will stay volatile for the foreseeable future but do not lose sight of this massive thematic shift in viewing media OTT. Please note that our outlook does not include the impact, if any, of new tariffs that may be imposed on foreign-sourced goods as there are still too many uncertainties related to the timing, scope and level of potential near-term changes in this area. We, along with our partners, are taking steps to mitigate potential adverse impacts.

A range of studies confirms the strength of Roku’s position in the U.S. marketplace. According to Kantar Millward Brown, Roku is the #1 TV streaming platform in the U.S. by hours streamed. Last month, Strategy Analytics reported that the Roku operating system powers 41 million OTT devices and smart TVs in the U.S. This is 36 percent greater than the next closest competitor and expected to grow. Recently released Parks Associates consumer survey data reveals Roku had 39% of the US streaming media player installed base as of Q1 2019. Below I’ve listed a few graphs that highlight what’s happening in streaming media.

Opinion

From a factor scoring perspective versus the other 199 brands in the brands index, here’s where Roku scores well as of 9/17/19:

90% 1YR sales growth

82% attractive margin expansion

98% in low debt to enterprise value - a strong quality measure

95% high 1YR sales growth

85% high 1YR EPS growth

94% top accelerating sales growth (1YR vs last 3YR average)

98% strong sales surprise last quarter

2% in low operating margins - this offers significant opportunity to continue increasing margins over time

Low scores in ROIC and ROIC over WACC also offer strong gains in efficiency once scale has been achieved. This will become a wonderful cash flow machine at some point as the cost of adding new customers drops and the recurring revenue begins to compund

11/6/2019:

The stock is down big after-hours but I would be shocked to see it stay down once people analyze the quarterly details and listen to the call. This company is in the driver seat for a major secular theme: the shift to streaming and the need for a simple user interface to navigate all the options. Yes it’s expensive, and for good reason. They are executing well, have enormous opportunities to ad more and pricier ad revenue as streaming becomes as prevalent as cable has been for 50 years. They made a big acquisition because they see the future of this business very clearly and have to be given the benefit of the doubt. They are just connecting the dots between consumer viewing trends, ad placement trends and automated ad sales trends. I’ll be buying this puppy on any dips in a market that does not like growth stocks right now. Once investors realize growth will not accelerate they will sell the cyclicals and value stocks with low growth and high valuations and come right back to companies that have higher and sustainable growth rates.

Old comments:

To say ROKU is misunderstood would be an understatement. That makes for a very volatile stock at times but if you can stand the VOL, ROKU could just be a big winner over the next 3-5 years. I’m surprised they haven’t already been acquired but the Founder & CEO doesn’t need the exit-event. Everything is for sale at the right price however. I have 3 Roku remotes and a Roku Smart TV, very few companies are on the list of being so prevalent in my household. If Im a normal customer, there’s lots of growth ahead. Bears will say there’s no moat with a dumb remote and I will agree but by that logic there’s no moat for so many other products and brands with significantly higher market caps that have become a standard part of life. The moat is customer adoption and being sufficiently pleased with the product/service that there’s no reason to consider switching. That’s called a network effect and Roku plays in one. The more consumers in the network, the more valuable the network becomes, the more recurring revenue and add-on services can be added. There’s currently 30million in the network now and growing well.

ROKU is clearly performing well in a fairly new category and they and investors should always expect competitive threats. I think the saving grace here is most companies are focused on building their own DTC streaming service, there’s few companies looking to be the platform that can deliver all of these DTC offerings to consumers in 1 place. The fact that 1 in 3 smart-tv’s are ROKU TV’s just makes the system the “one to beat” for competitors. Once you enjoy a service, you usually stick with it so I’ll be watching the TV sales like a hawk. Make no mistake, the streaming business is tough though, first you have to spend to acquire subscribers and viewers, then you earn the right to monetize all those people. ROKU is in spend mode and will continue to run virtually break-even until the inevitable free-cash flow cross-over point. In a tough category, Roku is carving out a niche as a key platform to gain access to all your video streaming options. I already subscribe to Netflix and Amazon Prime and YouTubeTV for my “cable” offering so I’m not buying add-on services through the Roku devices but based on earnings, lots of people are! The company has a high quality balance sheet and strong sales growth with a large total addressable market. Advertising inside streaming platforms is early and Roku is a leader in this fast growing market. The stock has been a strong performer and overall I think there’s great returns ahead. Caution sign: like most growth stocks, ROKU is NOT cheap at 13X sales and it’s a major momentum manager darling, they are fickle investors and when they leave, they do so with skid-marks. The irony, the actual streaming business isn’t nearly as volatile as Roku stock so do not lose sight of the big picture trends here, this is an unstoppable shift in the way consumers view media and Roku has a wicked lead and has built a solid brand with manufacturers, brands, and consumers. To reiterate, this puppy can be very volatile at times but when you see significant downside VOL, that’s usually a great time to start adding to the position.

As I add to this update, the stock has fallen from $172 to $105, technically it could fall back to the $77 break-out level but I’m happy to keep adding on big dips because I think this stock can still double at least over time.